Global Logistics Update

Blank Sailings on TPEB Surge; USTR’s Revised Plan Is Less Aggressive Than Expected

Updates from the global supply chain and logistics world | April 24, 2025

Global Logistics Update: April 24, 2025

Trends to Watch

Talking Tariffs:

U.S. Trade Representative (USTR) Releases Revised Fee Plan for Chinese Ships: Last Thursday (April 17), the USTR released a revised plan to impose fees on Chinese-built and Chinese-operated vessels. The plan is set to take effect on October 14, 2025. The revised plan, which is significantly less aggressive than the original proposal released in February, is expected to add less cost than initially expected.

New fees and restrictions will be implemented via a phased approach over time. The plan lays out upcoming vessel fees and restrictions across four Annexes:

- Annex 1: Incremental increases in fees on Chinese-owned or Chinese-operated ships, charged per U.S. voyage and based on the net tonnage of the vessel

- Annex 2: Incremental increases in fees on Chinese-built ships, charged per U.S. voyage and based on either net tonnage or the number of containers—whichever charge is greater

- Annex 3: Fees on all foreign-built car carrier vessels, not just those from China

- Annex 4: Beginning in 2028, incremental increases in restrictions on transporting liquified natural gas (LNG) via any foreign vessel

Fees and restrictions will not be cumulative, meaning each vessel will be subject to only one Annex at a time. Any applicable fees will be charged per vessel, and will apply per voyage to the U.S.

- U.S.-China Trade War Continues: Earlier this week, President Trump told reporters that the existing 145% IEEPA tariff on China “will come down substantially, but it won’t be zero.” However, this morning, a spokesman for China’s Ministry of Commerce stated that no tariff-related negotiations are taking place with the U.S., despite President Trump telling reporters yesterday that “everything’s active” when asked about talks with China.

Ocean: Trans-Pacific Eastbound (TPEB)

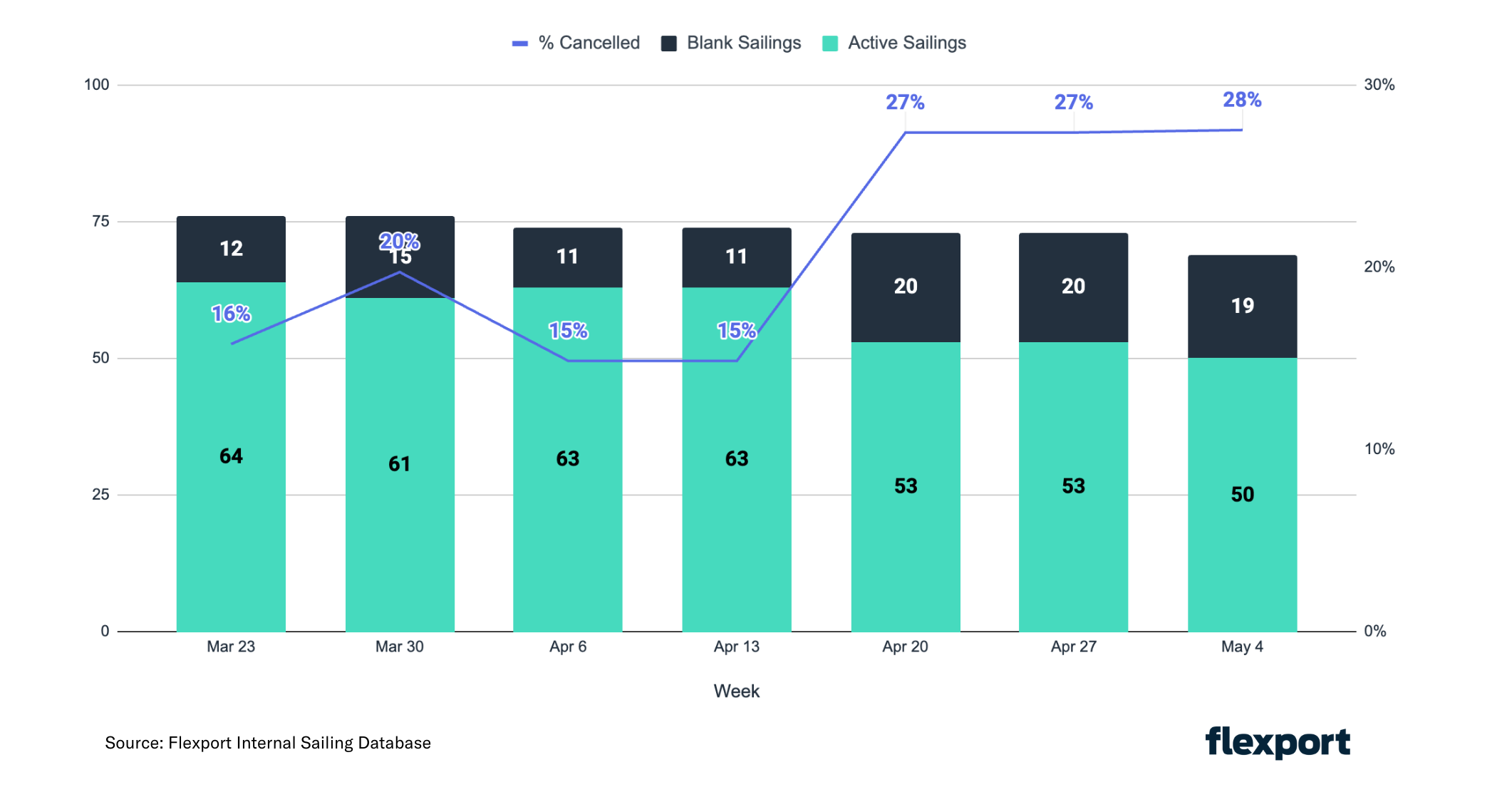

Capacity and Demand: The broader market is observing a significant negative impact on shipping volumes from China to North America, with 50% cancellations. The short-term outlook for volume growth from Southeast Asia to North America remains muted as we see consistent volume in April compared to January through March, roughly 6,000 TEUs.

Increased Blank Sailings: Ocean carriers are withdrawing capacity in the Transpacific Eastbound trade at faster rates than COVID in anticipation of reduced demand following new tariffs on shipments from China to the US. Carriers are reducing capacity by deploying smaller vessels, blanking (cancellation) scheduled sailings, and even the suspension of entire service loops. For context, a service loop is like a bus route. It’s a set schedule that ships follow every week, stopping at the same ports in the same order.

Ocean Alliance (CMA CGM, COSCO, Evergreen, and Orient Overseas Container Liner), Premier Alliance (ONE, HMM, YML) and ZIM/MSC have completely suspended eight of their weekly service loops. See Table 1 below. Additionally, more services are blanked for several weeks across alliances/carriers, with further blank sailing announcements expected. In late April and early May (Weeks 17-19), more than 25% of weekly service-loops are already cancelled. In comparison, Week 19 of 2020, during the early stages of COVID, had a 24% cancellation rate. Limited information is available for Week 20 and after, as carriers are closely monitoring market developments and may announce additional blank sailings depending on changes to demand. See our blog post for more details.

Table 1: Suspended Transpacific Eastbound Service Loops

| Carrier / Alliance | Service Loop | Suspension Period |

|---|---|---|

| Ocean Alliance | PRX / CP1 / PCS1 / PRX / AAS2 | Week 17 - 26 |

| Ocean Alliance | SEA3 / PSX | Week 18 - 23 |

| Ocean Alliance | CPS / AAC2 / HBB / PCN3 | Week 17 - 21 |

| Ocean Alliance | CBX / ECC3 / AWE7 / CBX | Week 16 - 24 |

| Mediterranean Shipping Company | ORIENT | Week 16 until further notice |

| ZIM | ZX2 | Week 16 until further notice |

| Premier Alliance | PN4 | Scheduled to begin in May, suspended until further notice |

| Premier Alliance | PS5 | Scheduled to begin in May, suspended until further notice |

- Equipment: Generally, container availability at origin ports in Asia for TPEB shipments remains good. Localized equipment shortages in Southeast Asia could still pose minor challenges for TPEB shipments originating from specific ports in that region. While not a major concern overall, it’s something to be aware of for shipments from those areas.

- Freight Rates:

- Floating Rates (GRI): Several carriers have announced a General Rate Increase (GRI) effective around May 1 for the TPEB market. However, the actual implementation and the magnitude of this GRI appear to be contingent on the volume of cargo coming out of Southeast Asia destined for North America. This suggests that if Southeast Asian volumes remain soft, the GRI may be a placeholder for now.

- Fixed Rates (Peak Season Surcharge): Several carriers have announced Peak Season Surcharges (PSS) for TPEB shipments, scheduled to take effect in the second half of May. As with the GRI, the application and extent of these surcharges will likely be influenced by the market response to the GRI in the first half of May, and overall demand on the TPEB route. Carriers are likely monitoring the situation before fully implementing these surcharges.

Ocean: Far East Westbound (FEWB)

- Capacity and Demand: Market demand remains flat, with no near-term boost in cargo volumes expected. The European Union’s ongoing interest rate adjustments support forecasts of a gradual recovery in European retail consumption. Far East manufacturers are increasingly redirecting their U.S.-bound inventories to the European market, which reinforces the outlook for stronger medium-to-long-term demand growth on the Europe route. Capacity oversupply persists on the Europe route. Upcoming additional U.S. port fees on Chinese vessels is accelerating the redistribution of capacity from Trans-Pacific routes, worsening the existing surplus in Europe-bound capacity. Blank sailings for Labor Day remain moderate, in line with demand trends. However, vessel schedule delays at ports of loading (POLs) could slightly impact cargo departing efficiency.

- Freight Rates: The Shanghai Containerized Freight Index (SCFI) has held steady for six weeks already, with stability likely extending through mid-May. Most carriers have confirmed that early May rates will remain unchanged from late-April spot levels.

Ocean: Trans-Atlantic Westbound (TAWB)

- Capacity and Demand: Congestion at the Ports of Piraeus, Mersin, and Valencia in the Mediterranean, as well as in Hamburg, Antwerp, Rotterdam, and Le Havre in North Europe, has led to service challenges and vessel delays. Antwerp terminals are shrinking their delivery window to decrease the number of containers at the terminal.

- Equipment: Equipment shortages persist in parts of Central Europe, particularly in Austria, Slovakia, Switzerland, Hungary, and Southern/Eastern Germany. Carrier haulage is recommended for these origins. No major issues in other ports and regions.

- Freight Rates: Due to the postponement of U.S. tariffs on the EU, carriers are anticipating a peak in demand for the next 90 days. Some carriers already implemented a PSS ex North Europe beginning May 13. In the West Mediterranean, the PSS that was planned for April will be applied in the beginning of May. In the East Mediterranean, carriers are implementing PSSs and GRIs at the beginning of May, as they anticipate demand to increase from Turkey, Greece, and Egypt.

Ocean: Indian Subcontinent to North America

- Capacity and Demand: Northwest India to U.S. East Coast routes are facing a capacity reduction of nearly 50% this week due to carriers’ blank sailings. These cancellations stem from operational issues (mispositioned vessels) and volume drops from tariffs, which did not materialize. Carriers now report robust demand for these routes in the coming weeks. Conversely, capacity to the U.S. West Coast is being cut due to blank sailings and adjustments driven by weak demand from China. Shipments from the Indian Subcontinent to China often rely on feeder networks connecting to mother vessels in the Chinese market.

- Freight Rates: Strong market demand is likely to drive rate increases from the Indian Subcontinent to the U.S. East Coast. If carriers raise rates for Southeast Asia, similar increases may follow for the U.S. West Coast in the near future.

Air Freight Update (Week 15: April 7 - April 13, 2025):

- Partial Post-Eid Recovery Masks Deeper Demand Concerns: Global tonnages rebounded +3% week on week (WoW) in Week 15 (April 7–13) after a -7% drop in Week 14. However, 2-week-on-2-week (2Wo2W) volumes fell -6%. The year-on-year (YoY) +9% increase is largely due to Eid timing last year, not genuine demand strength. Ongoing U.S.-China trade tensions are contributing to demand uncertainty and order cancellations.

- Average Global Rates Soften: Worldwide average air cargo rates dipped -1% WoW to $2.48/kg in Week 15, slowing 2Wo2W pricing growth to +2% (from +3% previously). YoY rates remained slightly positive at +2%. Trade friction and deferred sourcing decisions are weighing on price momentum, despite only a modest +1% 2Wo2W capacity increase.

- Regional Divergence in Volume and Rate Trends: Africa (+13%) and MESA (+12%) saw double-digit WoW volume rebounds post-Eid, while the Asia-Pacific rose +4%. Europe (-1%) and North America (-2%) volumes declined. Only North America registered a WoW rate increase (+4%), while MESA (-4%) and the Asia-Pacific (-2%) saw the largest drops, driven in part by low-rate intra-regional flows.

- Trans-Pacific Weakness Intensifies: Despite the Asia-Pacific’s +4% WoW growth, exports to the U.S. fell -3% for the second straight week, with China/Hong Kong volumes down -7%. No surge in ecommerce volumes has been observed ahead of the May 2 U.S. de minimis removal. Temporary U.S. tariff exemptions on laptops, phones, and semiconductors may provide some relief, but the outlook remains negative.

Source: worldacd.com

Please reach out to your account representative for details on any impacts to your shipments.

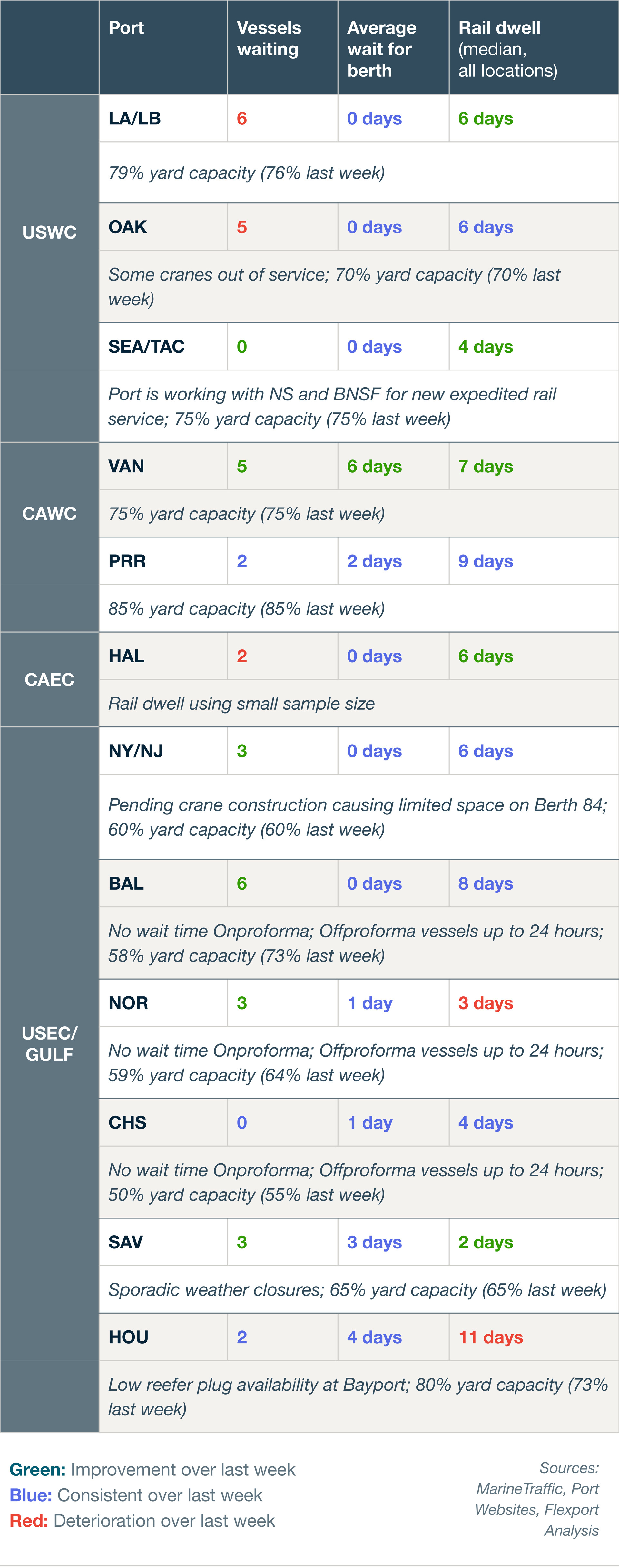

North America Vessel Dwell Times

Webinars

Tariff Trends 2025: Expert Insights on the New U.S. Customs Landscape (April 23, 2025)

Available on Demand

The Control Tower Advantage: Visibility, Agility, and Smarter Decisions

Tuesday, April 29 @ 7:00 am PT / 10:00 am ET / 15:00 BST / 16:00 CEST

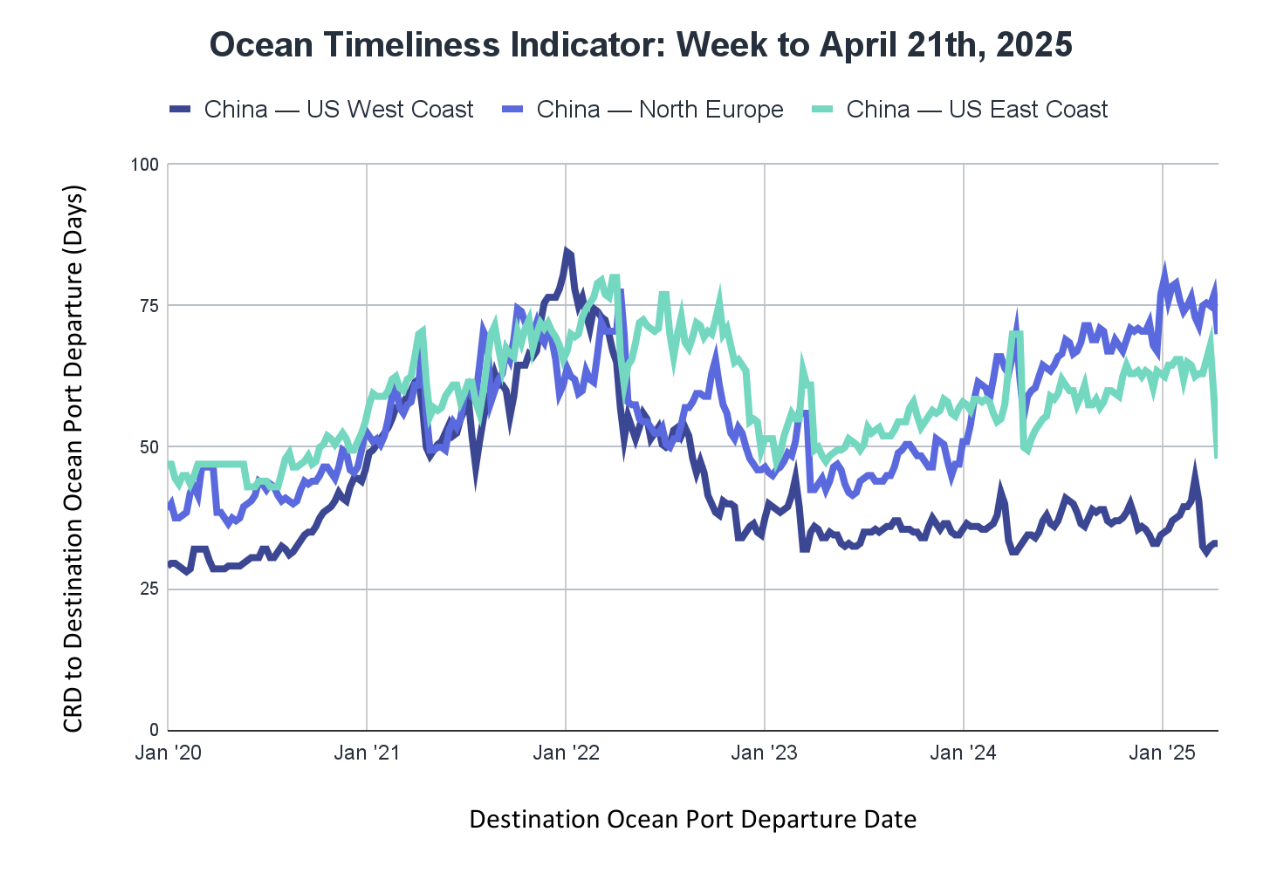

Ocean Timeliness Indicator

This week, the Flexport OTI for China to the U.S. West Coast remained stable, while China to North Europe and China to the U.S. East Coast dropped considerably.

Week to April 21, 2025

After a big drop on the Ocean Timeliness Indicator (OTI) for China to the U.S. West Coast in mid-March (-10 days), it’s now China to North Europe and China to the U.S. East Coast showcasing a steep fall, decreasing from 77 to 70 days and 58.5 to 48 days, respectively. Meanwhile, China to the U.S. West Coast remained idle at 33 days this week.

About the Author

Sign up for Global Logistics Update

Related content

Ready to get started?

Learn how Flexport’s supply chain solutions can help you capture greater opportunities.